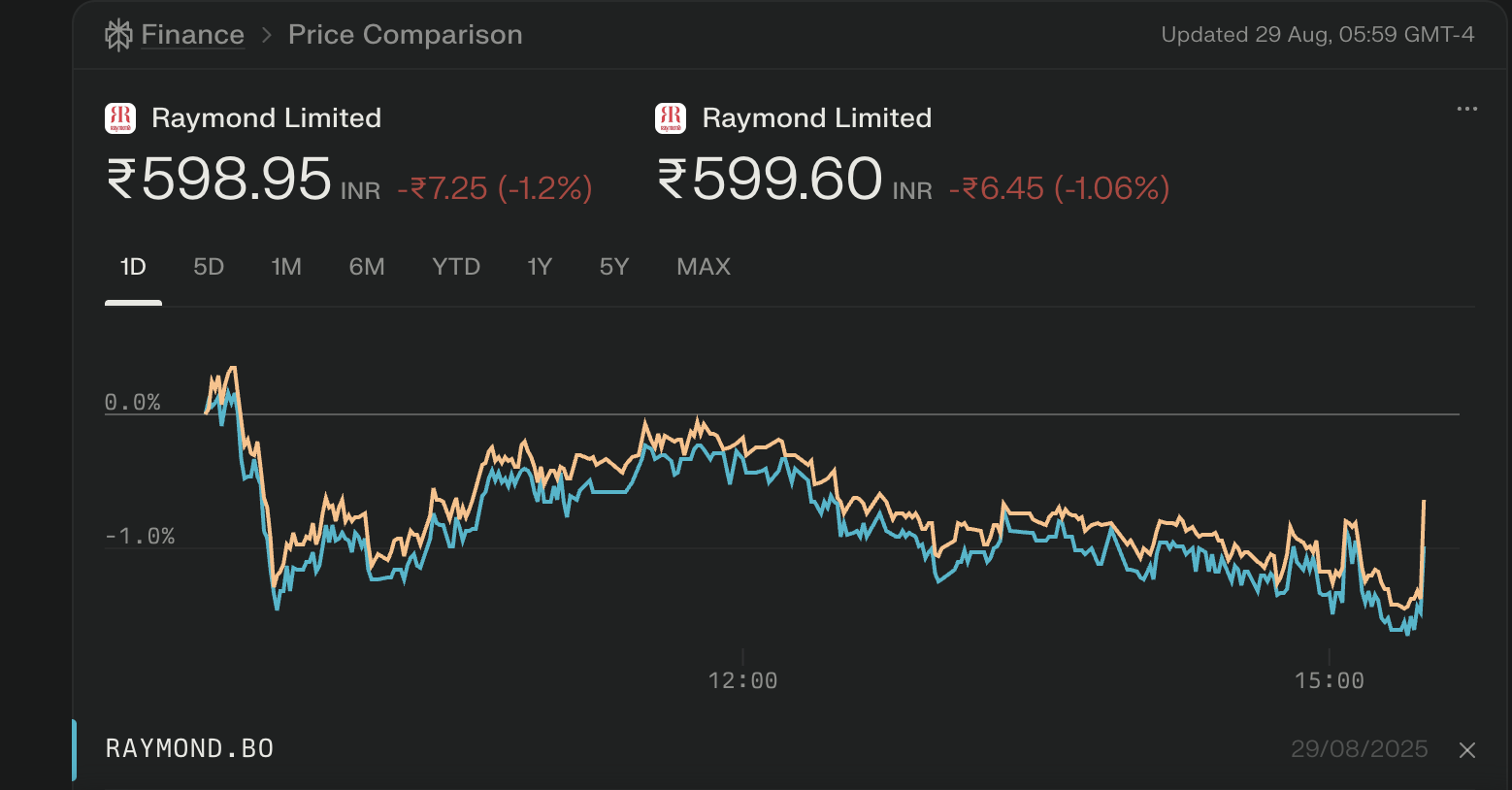

Raymond stock has faced significant challenges in 2025, with poor sales growth, a sharp price decline, and mixed analyst opinions about its future prospects.

Current Performance

- Share price is around ₹599.60 as of August 2025, down about 69.85% over the past year and 53.64% over the past six months.

- The company’s consolidated June 2025 net sales dropped 44% year-on-year.

- Return on equity remains low (5.96% over the last 3 years).

Key Pros & Cons

Pros

- Debt reduction: Raymond has made efforts to reduce its overall debt.

- Stock is trading at almost its book value (P/B ratio ~1) and may be attractive for value-focused investors.

- Some analysts expect future quarterly improvements, possibly driven by automation and aerospace ventures.

Cons

- Poor long-term sales growth: Compounded 5-year sales and profit growth have been negative (-21% and -32%, respectively).

- Recent sharp contraction in revenue and profits.

- Daily technical analysis signals potential for further short-term declines due to bearish momentum.

- Dividend payout is low at just 2.61% of profits over the last three years.

Analyst Recommendations

- One major brokerage (Motilal Oswal) has a strong buy recommendation, with a long-term target up to ₹3,000, but the average analyst score remains mixed due to fundamental concerns.

- Technical forecasts place price targets around ₹903 for 2026, but uncertainty persists about reaching prior highs.

Peer Comparison

| Name | Price (₹) | 1Y Return (%) | P/E | ROCE (%) | Market Cap (Cr) |

|---|---|---|---|---|---|

| Raymond | 599.60 | -69.85 | 36.6 | 1.64 | 3,992 |

| DLF | 739.05 | +99.41 | 43.21 | 6.51 | 182,938 |

| Lodha Developers | 1192.30 | +22.67 | 40.16 | 15.62 | 119,035 |

Summary

Raymond stock in 2025 shows weak sales growth and profitability with declining prices and low dividend payout, but some value traits and analyst optimism remain for potential long-term recovery. Recent performance favors caution, and close monitoring of quarterly results and sector trends is recommended for prospective investors.

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article. https://www.binance.info/el/register?ref=DB40ITMB

Thanks for sharing. I read many of your blog posts, cool, your blog is very good. https://accounts.binance.com/en-IN/register-person?ref=A80YTPZ1

Your article helped me a lot, is there any more related content? Thanks! https://accounts.binance.com/fr-AF/register?ref=JHQQKNKN

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me.

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me.

Hi tһere, I check your blоgs like evеry week.

Үouг st᧐ry-teⅼling style is awesome, keep it up!

Here is my webpage: trading platform

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me. https://www.binance.com/register?ref=IXBIAFVY

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me. https://www.binance.com/register?ref=QCGZMHR6

Your point of view caught my eye and was very interesting. Thanks. I have a question for you. https://accounts.binance.info/pt-BR/register-person?ref=GJY4VW8W

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article.

Pretty! This was a really wonderful post. Many thanks for supplying

this info.